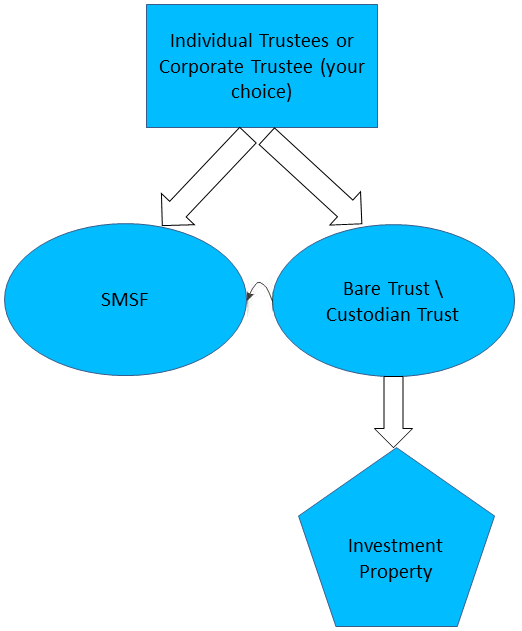

Related party loan is where the SMSF borrows money from a related party who is a Member or an associate of a Member of the SMSF. To secure the loan, a typical structure is required to set up as below:

The structure for the related party loan can be more cost effective. The related party loan can be simply held by the Bare Trust/Custodian Trust with Individual Trustees. Unlike a related party loan, if the SMSF intends to buy properties with bank loans, a Corporate Trustee and a Custodian Trustee are required to be set up by most Banks.

When we set up the related party loan structure for your SMSF, we will provide you with all the necessary documentation and also a loan schedule showing the loan details and the monthly repayment. The sample loan repayment schedule is noted below:

Sample Loan Repayment Schedule

Arm’s Length & Commercial Terms

It’s important to ensure the terms of lending to the SMSF are on an arms-length basis and issued on commercial terms. This means the Members need to charge a reasonable amount of interests on the loan to the SMSF. The ATO provides the annual LRBA safe harbour interest rates as noted in the table below:

| Year | Real Property | Listed Shares or Units |

| 2024 – 2025 | 9.35% | 11.35% |

| 2023 – 2024 | 8.85% | 10.85% |

| 2022 – 2023 | 5.35% | 7.35% |

| 2020 – 2022 | 5.10% | 7.10% |

| 2019 – 2020 | 5.94% | 7.94% |

| 2018 – 2019 | 5.80% | 7.80% |

| 2017 – 2018 | 5.80% | 7.80% |

| 2016 – 2017 | 5.65% | 7.65% |

Conditions and circumstances for borrowing for an SMSF

A limited recourse borrowing arrangement (LRBA) involves an SMSF Trustee taking out a loan from a third-party lender. The Trustee has to use those funds to purchase a single asset (or collection of identical assets that have the same market value) to be held in a separate Trust. It is crucial to note that, an SMSF does not allow to purchase of any residential properties from a related party. The ATO provides the annual LRBA safe harbour interest rates for the unit assets under the loan.

The returns earned from the asset go to the SMSF Trustee. In case if the loan defaults, the lenders’ rights are restricted to asset apprehended in the separate trust. This means there is no recourse to the other assets held in the SMSF. An SMSF loan can be used to buy investment property. The returns on the investment – whether that’s rental income or capital gains – are funnelled back into the super fund, increasing your retirement savings.