A Transition to Retirement Pension is an income stream that you can commence from your SMSF if you have reached preservation age and are still working. With a Transition to Retirement, you may be able to reduce your working hours without reducing your income. This can be done by topping up your part-time income with a regular ‘income stream’ from your SMSF.

Until recently, you could only access your SMSF balance once you turned 65 or retired. This means it was difficult to reduce your work hours and still maintained your standard of living. Transition to Retirement allows you to withdraw some or all of your SMSF balance into a retirement income stream.

How does a Transition to Retirement work?

You will have 2 accounts within your SMSF. Once you reach preservation age, you can elect to have a Transition to Retirement income from your SMSF.

If you are 55 then you have to take as an income of between 4% – 10% (3% minimum for 2013 year) of this Transition to Retirement balance. The first year of the Transition to Retirement is calculated on a pro-rata basis, using the days in the year.

How do you activate a Transition to Retirement?

Trustees manage the SMSF and are responsible to start the Transition to Retirement. When you start the Transition to Retirement, minute this decision. Here is a template of these minutes.

Then send a copy of the minutes to Superannuation Warehouse via the email address.

Tax consequences in the SMSF

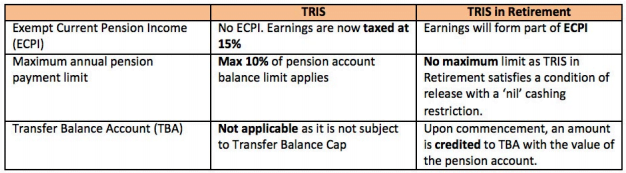

Starting from 1 July 2017, all Transition to Retirement income will be taxed at a rate of 15%. This update is made in the 2016-2017 Federal Budget.

Tax on the Transition to Retirement income received from the SMSF

If you are over age 60, the income you receive in the form of pension payments from your SMSF are tax-free in your hands. If you are between age 55 and under age 60, this Transition to Retirement income should be included in your personal taxable income.

Payments cannot be lump sums

The pension payments that you receive do not have to follow any set pattern (e.g. monthly or quarterly etc) even though most do. You just need to make sure that at least the minimum amounts of Transition to Retirement payments have been made over the year.

Minimum Drawdown Amount

Depending on your age, there is a minimum that should be withdrawn each year from the Transition to Retirement balance. At the start of the year, calculate the market value of the Transition to Retirement. The minimum drawdown depends on your age. See the preservation age table for the percentage.

| Age | Minimum % withdrawal for the 2008–09, 2009–10 and 2010–11 income years for certain pensions and annuities | Minimum % withdrawal for the 2011–12 and 2012–13 income years for certain pensions and annuities | Minimum % withdrawal for the 2019-2023 income years | Minimum % withdrawal (in all other cases) |

| Under 65 | 2% | 3% | 2% | 4% |

| 65–74 | 2.50% | 3.75% | 2.50% | 5% |

| 75–79 | 3% | 4.50% | 3% | 6% |

| 80–84 | 3.50% | 5.25% | 3.50% | 7% |

| 85–89 | 4.50% | 6.75% | 4.50% | 9% |

| 90–94 | 5.50% | 8.25% | 5.50% | 11% |

| 95 or more | 7% | 10.50% | 7% | 14% |

Due to the global financial crisis, the minimums were temporarily halved for the 2009 – 2011 financial years. This is known as minimum pension drawdown relief.

Another 50% reduction was introduced as a response to COVID-19 crises in the 2020 and 2021 financial years. For further guidance, please see here.

PAYG Registrations

An SMSF must register for PAYG when a Transition to Retirement is started. You can download the online calculator to calculate the PAYG withholding tax for annual amounts or for regular payments.

Access the ATO website for tax tables to see weekly, fortnightly, monthly or quarterly tables from the ATO website.

We will register your SMSF for PAYG withholding tax.

Your Peace of Mind

Superannuation Warehouse is based in Melbourne and have clients throughout Australia. We deliver our SMSF administration services in an efficient and paperless way. This efficient service means a competitive fee to you. Our low ongoing fees will enable you to take control of your Super.

General Advice

Superannuation Warehouse is an accounting firm and do not provide financial advice. All information provided has been prepared without taking into account any of the Trustees’ objectives, financial situation or needs. Because of that, Trustees are advised to consider their own circumstances before engaging our services.

Follow us:

Recent Posts

Info Pages

Popular Searches

Address

Phone

Opening Hours

Monday to Friday

9.00am – 5.00pm

© 2010 - 2024 Superannuation Warehouse : All Rights Reserved

Digital Strategy by